GREAT BAY--Minister of Finance Marinka Gumbs on Monday delivered a detailed presentation in a Central Committee meeting of Parliament on five draft harmonized national ordinances on financial supervision, explaining that the legislation is essential to preserving St. Maarten’s financial stability, protecting its international standing, modernizing parts of the financial sector, and ensuring continued compliance within the monetary union with Curaçao.

In her presentation, the Minister first placed the proposed legislation within its constitutional context, explaining that because Curaçao and St. Maarten form a monetary union, both autonomous countries are required to enact uniform national ordinances governing key areas of the financial sector.

Minister Gumbs stressed that these laws are called “uniform national ordinances” for a reason. She explained that neither Curacao or St. Maarten can unilaterally amend the financial supervisory framework, because any change must be passed in identical wording by both parliaments in order to remain valid. She described this as a constitutional safeguard tied to the nature of the monetary union.

At the same time, the Minister emphasized that uniformity does not mean one country is subordinate to the other. She said the system is based on equality, with neither Curaçao nor St. Maarten having superior powers over the other, and that the joint framework exists so the CBCS can carry out its responsibilities consistently in both countries while still respecting the constitutional autonomy of each country.

She told Parliament that maintaining a uniform statutory framework serves several objectives, including promoting the stability, soundness, and integrity of the financial system, safeguarding legal certainty, ensuring equal competitive conditions for supervised institutions, and preventing regulatory divergence between the two countries.

The Minister also used her presentation to explain the meaning and implications of “grey listing,” warning that if St. Maarten fails to address deficiencies identified by international evaluators, the country could be placed under increased monitoring by the Financial Action Task Force (FATF). She said grey listing signals weaknesses in a country’s anti-money laundering and counter-terrorist financing framework and can lead to higher transaction costs, reputational damage, and pressure on international payment traffic and correspondent banking relationships.

Minister Gumbs said the five draft laws before Parliament are necessary to keep St. Maarten aligned with international standards and to avoid that risk.

She then outlined the purpose of each of the five draft ordinances.

The first, the Draft National Ordinance on the Supervision of Securities Intermediaries and Asset Managers, is intended to close a gap in St. Maarten’s legal framework. The Minister said that while banks, insurers, and pension funds are already supervised, securities intermediaries and asset managers are not currently subject to a specific supervisory regime. In a fast-moving and increasingly digital financial environment, she said, that gap could attract undesirable activity.

The proposed law would introduce a licensing requirement, place these entities under prudential and conduct supervision, and provide the CBCS with the legal tools needed to monitor compliance. Minister Gumbs said this would strengthen investor protection, market integrity, and confidence, while also supporting investment, entrepreneurship, and long-term economic growth. She noted that the draft aligns with international norms, including standards associated with the International Organization of Securities Commissions (IOSCO), and said the corresponding law already entered into force in Curaçao on June 17, 2017. In St. Maarten, she said, the draft has now been submitted to Parliament for approval.

The second, the Draft National Ordinance on the Supervision of Virtual Asset Service Providers, was described by the Minister as a necessary response to international developments. She said that in 2018, the Caribbean Financial Action Task Force (CFATF) amended Recommendation 15 to require countries to regulate and license virtual asset service providers for anti-money laundering, counter-terrorist financing, and counter-proliferation financing purposes. In 2024, Curaçao and St. Maarten were evaluated and found non-compliant because there was no statutory licensing requirement in place.

Minister Gumbs said the proposed law would introduce that requirement and place virtual asset service providers under the supervision of the CBCS. It would also strengthen compliance obligations, transparency of ownership, record keeping, and enforcement. She added that the draft contains important consumer protection safeguards, including the segregation of client funds and the protection of virtual assets held in custody. While virtual assets are now part of the modern financial landscape, she said, the country’s duty is to regulate them in a careful and proportionate manner.

The third, the Draft National Ordinance on the Oversight of Payments and Securities Settlement Systems, differs from the traditional supervisory laws, the Minister said, because it focuses not on individual institutions but on systems as a whole. She explained that the ordinance would create the legal basis for oversight of payment and securities settlement systems, which are critical to the functioning of daily transactions and the broader financial system.

Minister Gumbs said the law would formally anchor two core tasks of the CBCS: oversight of payment and securities settlement systems, including enhanced oversight of systemically important systems, and the bank’s catalyst function in promoting modernization, innovation, and cooperation in the financial sector. She stressed that in an age of digital payments, fintech innovation, and rising cyber risks, this kind of system-wide oversight is essential.

A major theme of her explanation was financial inclusion. She said the ordinance recognizes financial inclusion as a public interest and seeks to ensure that as cash use declines and electronic payments expand, individuals and small businesses are not left behind. She pointed specifically to Article 42E, which would empower the central bank to establish reasonable and equal conditions for users of payment and securities settlement systems. The Minister said financial inclusion is not only an economic goal, but a social imperative. She noted that this draft has been discussed in Curaçao, including in the summer of 2025, but has not yet passed there.

The fourth, the Draft National Ordinance on the Supervision of Operators of Financial Market Infrastructures, is aimed at securing St. Maarten’s payment and securities infrastructure in line with the global standards established under the CPMI-IOSCO Principles for Financial Market Infrastructures (PFMI). Minister Gumbs said compliance with these standards is no longer optional if St. Maarten wishes to remain fully connected to the international financial system.

She explained that clearing and settlement systems are the backbone of the country’s payment and securities infrastructure. If those systems do not meet international standards, St. Maarten risks financial and operational vulnerabilities, reputational damage, and in the worst case, exclusion from international correspondent banking networks. The draft law, she said, would integrate the relevant PFMI standards into national legislation, provide a statutory basis for supervision of financial market infrastructure operators, ensure compliance with international requirements, and help address shortcomings identified in the latest CFATF evaluation.

The Minister said the law would also formally assign to the CBCS the statutory task of establishing and operating national settlement systems for payments and, where needed, securities such as government bonds. At present, she noted, the payment settlement system operates on the basis of private law agreements with participating institutions, which is no longer sufficient given its importance. The proposed ordinance would also establish a framework for financial market infrastructure systems operated by private sector entities, including clear rules for authorization, access, supervision, and exemptions. According to the Minister, this draft has not yet been submitted to the Advisory Council in either Curaçao or St. Maarten.

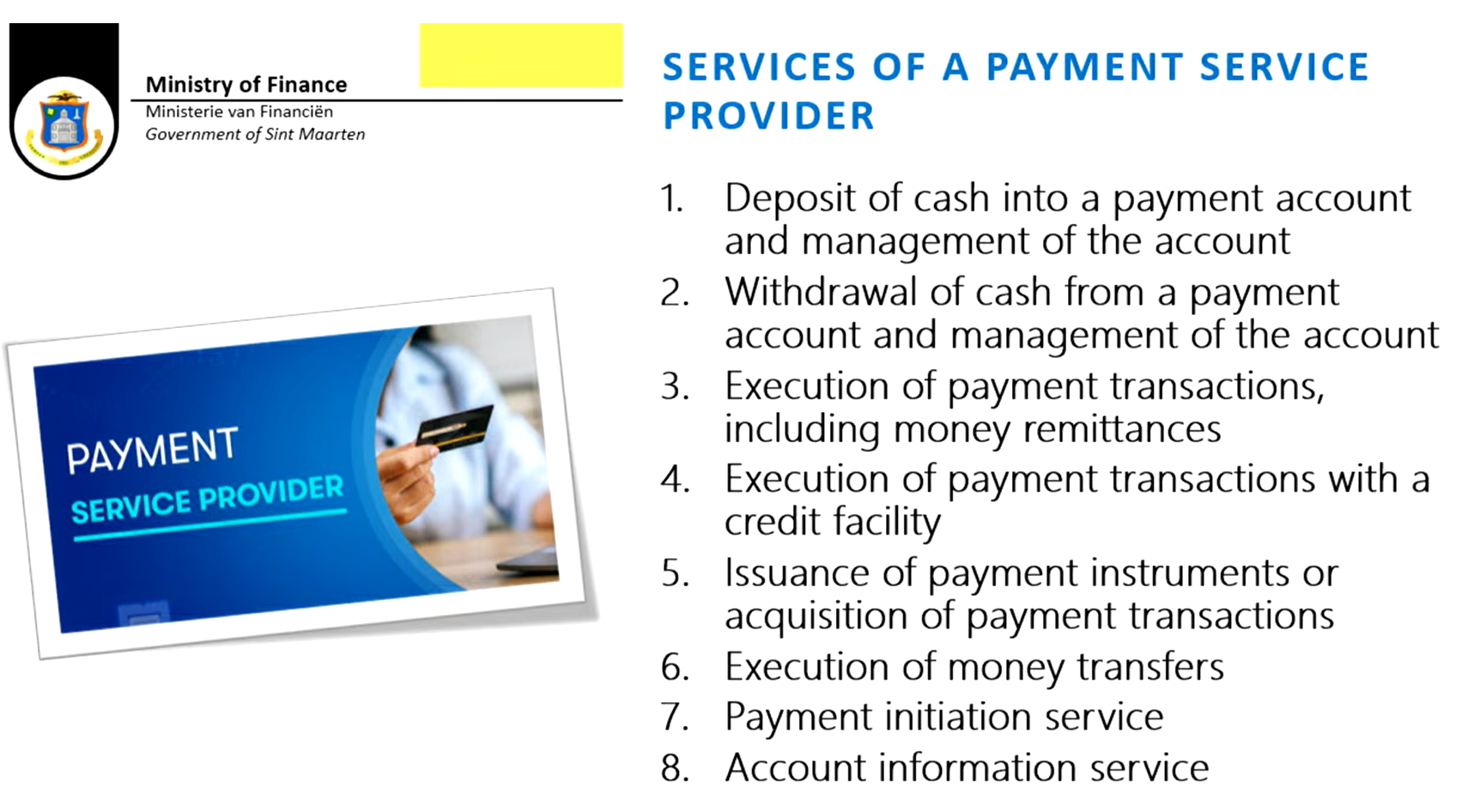

The fifth, the Draft National Ordinance on the Supervision of Payment Service Providers, was described by Minister Gumbs as the draft law with the most direct impact on the people of St. Maarten. She said the legislation would open the door to more affordable, modern, and innovative methods of financial service provision, particularly by enabling the licensing of payment service providers in St. Maarten.

She pointed out that residents on the French side already have access to significantly more digital payment services, and said this law would help make similar services possible on the Dutch side once qualified providers obtain a license. She framed the legislation as part of the government’s broader policy on financial inclusion, linking it to a 2015 United Nations General Assembly resolution recognizing financial inclusion as a prerequisite for sustainable development under Sustainable Development Goals 8 and 10.

The Minister described the proposed law as “step two” in a broader process, with the adoption of the Basic Banking Law in January being step one. She said step three would involve negotiating with and encouraging local and foreign market parties to offer services in St. Maarten, while step four would involve the licensing of providers that meet all legal requirements.

The draft would create a licensing regime for entities that wish to operate professionally or commercially as payment service providers in or from St. Maarten. Minister Gumbs said the law closely aligns with the eight existing national ordinances governing financial supervision and must remain substantively identical to the corresponding law in Curaçao because it is also a uniform national ordinance.

She said modern payment services would save time, reduce frustration caused by delayed or incorrect payments, lower transaction costs, reduce administrative burdens, increase automation, improve service quality, and contribute to a more efficient economy. She noted that digital payment services have lagged in St. Maarten partly because international providers must be able to show they are supervised in every country where they operate. If there is no local licensing framework, those providers become subject to enhanced supervision in their home jurisdictions.

To address that, the draft law introduces clear licensing rules, effective supervision by the central bank, and safeguards such as the strict segregation of client funds from the provider’s operating funds. The CBCS would assess providers against solvency, liquidity, reliability, integrity, security, and consumer protection requirements. The Minister said that stronger confidence in digital payment services would reduce reliance on cash, bringing savings for banks and merchants alike in areas such as security, cash transport, and staffing.

She also outlined the types of services that could be offered under the law, including cash deposits and withdrawals from payment accounts, execution of payment transactions and money remittances, payment transactions linked to a credit facility, issuance of payment instruments, money transfers, payment initiation services, and account information services. She noted that payment initiation services would allow a consumer or business to initiate a payment from an account held at another bank, which could be particularly useful for online purchases, while account information services could give consumers and businesses a consolidated view of multiple accounts in a single application.

Minister Gumbs reminded Parliament that the CBCS already has responsibility for supervising financial institutions in both countries, and that one of its key roles is to safeguard the continuity and availability of payment systems in order to maintain confidence in the common currency and the broader financial sector. She also stressed that compliance with FATF recommendations is critical because international payments and credit card transactions can be disrupted if a country is placed on a grey list or blacklist.

Summarizing the legislative position of the five drafts, the Minister explained that the first two drafts have already been finalized following approval by the Parliament of Curaçao. As a result, the scope for substantive amendment by the Parliament of St. Maarten is limited, and Parliament’s decision on those two measures is effectively whether to approve or reject them. By contrast, she said, Parliament retains full legislative authority over the remaining drafts, and once St. Maarten approves them, the text will be fixed for Curaçao’s corresponding parliamentary process as well.

Join Our Community Today

Subscribe to our mailing list to be the first to receive

breaking news, updates, and more.