GREAT BAY, St. Maarten--New survey findings published by the Centrale Bank van Curaçao en Sint Maarten (CBCS) show a construction sector that remains active but was increasingly cautious about 2025, with firms pointing to skilled labor shortages, rising logistics and material costs, and local infrastructure constraints as key pressures on performance and investment.

The 2025 Construction Sector Survey, conducted among registered construction companies during August and September 2025 and published in February 2026, provides a snapshot of recent business conditions, operational challenges, pricing expectations, and investment plans. The CBCS notes that the survey is designed to support its economic analyses and forecasts.

While the executive summary describes construction in both countries as dominated by micro and small enterprises facing cost pressures and skilled labor gaps, St. Maarten respondents expressed a more guarded outlook than their counterparts, with many anticipating weaker economic conditions and reduced investment activity.

A small-firm sector concentrated in core construction activity

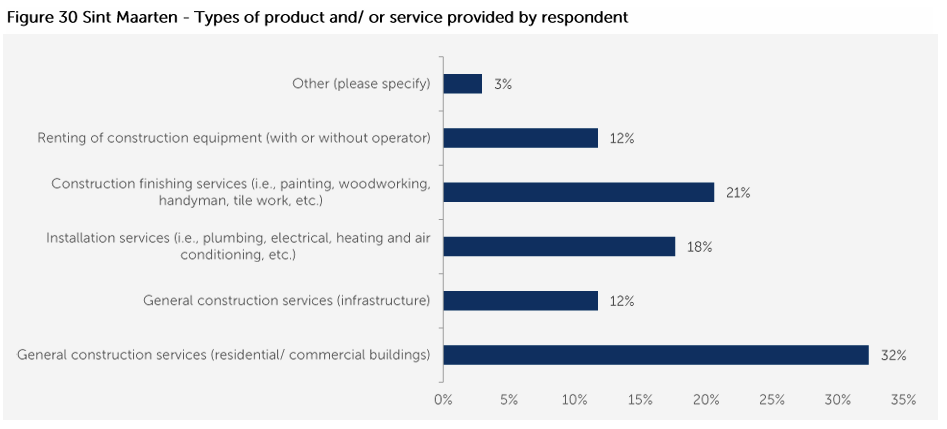

St. Maarten construction firms reported that their main lines of work are:

- General construction for residential and commercial buildings (32%)

- Finishing work (21%) such as painting, woodworking, and tile work

- Installation services (18%) including plumbing, electrical, and air conditioning

- Infrastructure-related general construction (12%) and equipment rental (12%)

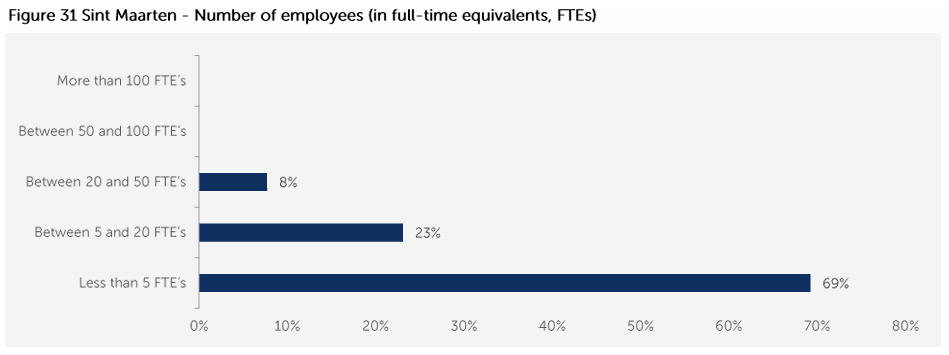

The sector is overwhelmingly small in scale: 69% of surveyed firms employ fewer than five full-time equivalents, 23% employ 5–20, and 8% employ 20–50, with no respondents reporting more than 50 full-time equivalents.

Domestic focus, imported inputs, and short inventory cycles

Most firms reported operating almost entirely within the local market, with 92% focused on domestic activity and 8% indicating exports or services abroad. At the same time, 46% reported importing materials or services, underscoring exposure to global supply chains and shipping costs.

Inventory practices reflect tight procurement cycles: 54% reported holding less than one month of inventory, while 23% indicated inventory was not applicable to their model, consistent with project-based, just-in-time operations.

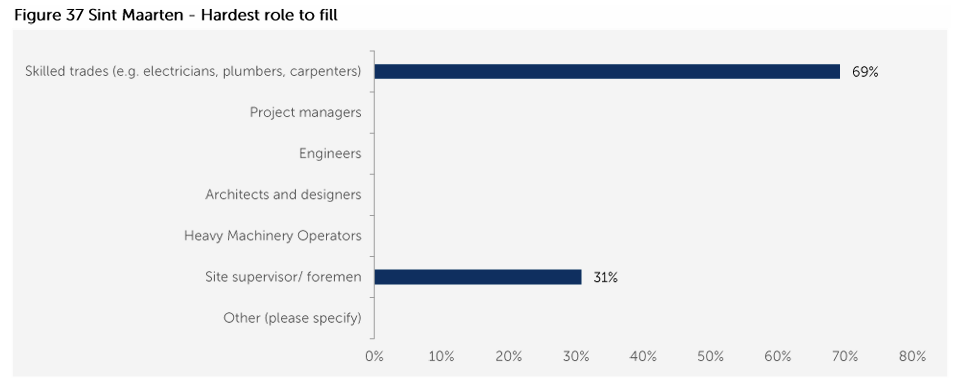

Labor shortages remain a core constraint

More than half of respondents (54%) reported difficulty finding workers. Recruitment challenges are concentrated in trades and on-site supervision: 69% identified skilled trades as the hardest roles to fill, and 31% cited difficulty hiring site supervisors or foremen.

Most firms expected their own staffing levels to remain steady in 2025, with 60% anticipating no change and 20% expecting some growth. Wages were also expected to be largely stable, with 60% forecasting no change and 40% expecting increases mainly in the 5–15% range.

Views of the broader economy were significantly more cautious: 50% of St. Maarten construction firms expected economic conditions to worsen in 2025 compared to 2024, while 30% anticipated improvement and 20% expected no change. Expectations for overall employment mirrored that caution, with 40% forecasting a decline, 40% stable conditions, and 20% an increase.

Business climate and market position: subdued sentiment

Respondents were similarly restrained regarding the business climate and their own market position:

- Business climate: 40% expected no change, 40% expected worsening, 20% expected improvement

- Local market position: 40% expected decline, 30% no change, 30% improvement.

Inflation, financing uncertainty, and higher logistics costs

Inflation expectations were heavily tilted upward: 70% expected inflation to rise in 2025. Financing expectations were mixed, with 40% expecting financing costs to increase, 10% expecting stability, and 50% reporting no clear view.

Firms broadly anticipated higher transportation costs: half expected international transportation costs for construction materials and equipment to rise by 10% or more, with similar upward expectations for local transportation. No respondents expected declines in either category.

Material and construction prices was expected to rise

All surveyed firms expected construction material prices to increase in 2025, most commonly in the 5–10% range (40%), with 30% expecting increases of 15% or more. The most frequently cited driver was transportation and shipping costs (50%), followed by other factors such as rising global demand and geopolitical tension.

Price expectations for construction work also pointed upward:

- Residential construction: 60% expected increases of at least 5%, 30% expected smaller increases, 10% expected prices to remain unchanged, none expected declines. Drivers cited most often were materials (50%) and skilled labor (30%).

- Construction Survey Report 2025…

- Non-residential construction: 80% expected price increases, with materials again the dominant driver (60%), followed by skilled labor (20%).

Investment plans: conservative in 2025 and restrained through 2030

Capital investment expectations for 2025 were notably cautious: 50% anticipated a decline in investment, 40% expected stability, and only 10% expected an increase. A large majority (90%) reported no planned capital investments for 2025.

Looking ahead to 2026–2030, 56% reported no planned capital investments, while others anticipated modest annual spending, most commonly below Cg 100,000, with a smaller share projecting higher annual investment ranges.

What firms say would help most

When asked about the main challenges currently facing St. Maarten’s construction sector, respondents prioritized:

- Skilled labor shortages (44%)

- Island infrastructure constraints (33%)

- Rising material costs (22%)

For improving the business climate, the top priorities were:

- Improved access to credit (33%)

- Strengthening the skilled labor pool (33%)

followed by reducing red tape and lowering the cost of doing business.

Caribbean context

St. Maarten’s results reflect pressures that are familiar across many small Caribbean markets: high exposure to shipping costs and import-dependent supply chains, persistent competition for skilled trades, and investment decisions that can tighten quickly when financing becomes expensive or uncertain. At the same time, construction remains a critical link in broader development, from housing and commercial buildout to resilience upgrades that help islands withstand climate-related shocks, which often raise the importance, and the cost, of building right the first time.

The survey report can be downloaded below

Join Our Community Today

Subscribe to our mailing list to be the first to receive

breaking news, updates, and more.